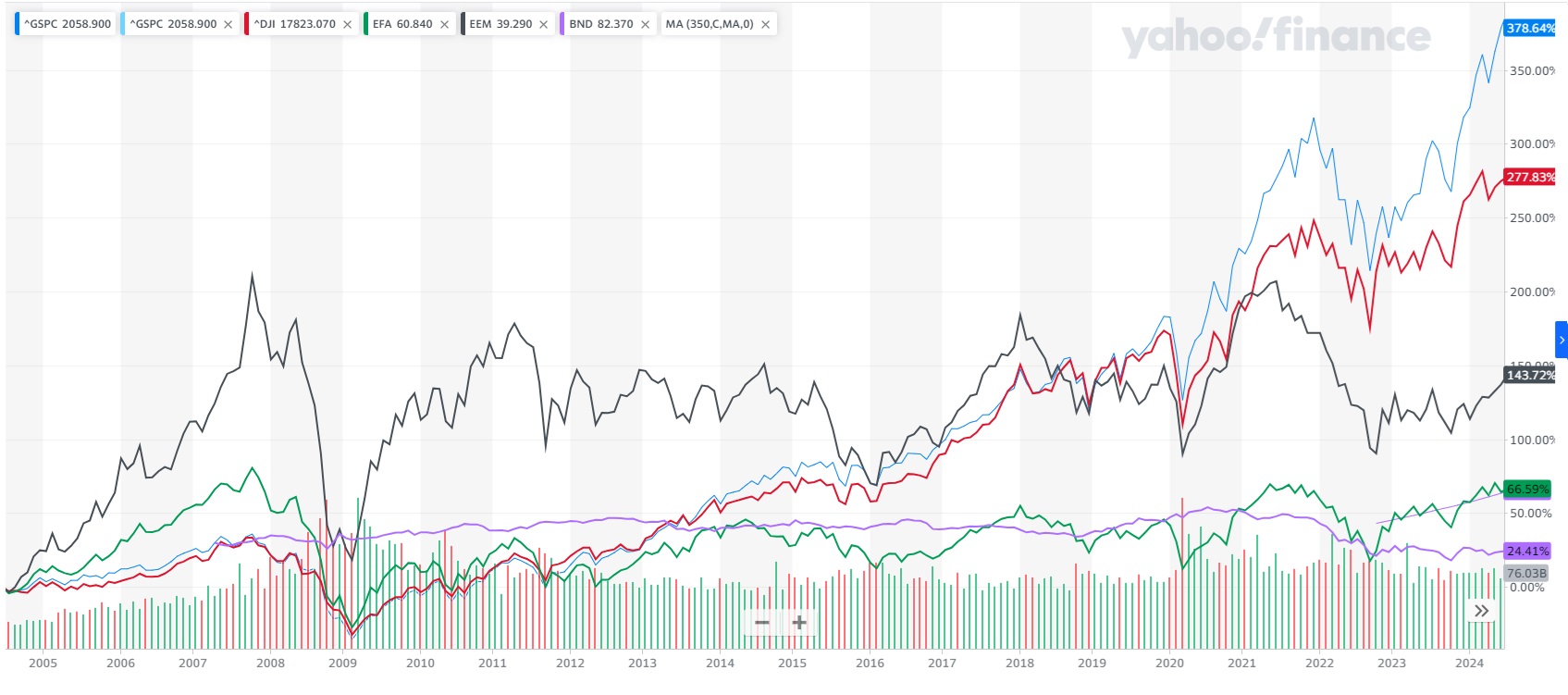

It is undeniable that US Equity Markets have delivered the highest returns over the past 20 years, with the DOW industrials delivering a 6.9% annualized compounded price return (red line in Chart I below), and the broader S&P 500 delivering 8.1% (blue line in Chart I). Further, it is impressive to see how a 7-8% annual return can compound to 275-375% over a 20-year period.

While Emerging Markets were the darling of the early 2000s, they only delivered 4.6% annualized over the full 20-year period, and have been completely flat at 0% for the past 15 years (black line in Chart I)!

Other laggards included Foreign Developed Markets (green line in chart I > 2.6% annualized over 20 years) and lastly US Bonds which had the lowest total returns (purple line in Chart I).

Chart I – 20 Year Market Returns (Source: Yahoo! Finance)

So what happened?

Why did the US dominate the world markets so handily?

Put simply, it is our opinion that corporate profits and valuations increased more rapidly than anywhere else on the planet. Here are some reasons why:

Low Inflation and Interest Rates: The U.S. maintained low inflation and interest rates for an extended period, allowing companies to borrow cheaply and leverage their balance sheets. This enabled them to pursue growth opportunities and generate significant profits, while also allowing investors to leverage their investments, driving valuations higher.

Government Stimulus: The U.S. government injected unprecedented and massive stimulus into the economy during downturns and even during upswings, providing a boost to corporate profitability and market valuations.

Innovation and Competitive Edge: U.S. companies led the way in innovation across various sectors, including internet development, software as a service, horizontal drilling, fracking, and artificial intelligence, outpacing their global competitors.

Regulatory Environment: Political activity and favorable regulatory changes significantly contributed to the rise in corporate valuations and profits, especially since the 2000s. Lobbying and political campaign spending resulted in regulatory changes that benefited businesses, particularly in politically influential industries like pharmaceuticals, petroleum, and communications.

So while this dominance has persisted over the past 5-10 years, will it continue?

The evidence appears mixed.

On the one hand, US relative advantages in the tech space and in the natural gas energy space appear to be secular in nature and hence should be long-lasting.

On the other hand, interest rates have now risen to more normalized levels, slowing down investment and in some cases causing major issues (e.g. debt refinancing in the corporate real estate sector). The US government also has fewer resources for stimulus and may consider austerity at some point. Labor costs are starting to rise once again, along with other inflationary inputs. Finally, equity market valuations are starting today at a much higher place than they were 20 years ago (Shiller PE is at 36 today vs was at 25 twenty years ago).

It is our belief that the current US Equity run can continue ahead in the near-term due to technical reasons, but that a continued 8%+ US equity annualized return is a lower likelihood possibility in the decades ahead. That said, there are several sustainable sectors that may persist with 8%+ annualized returns. For example, industrial businesses that have natural gas as a major input and are using greater automation relative to a traditional workforce, are today trading at low multiples but likely have a decade of competitive advantage ahead. Certain southeast Asian emerging market countries are “emerging” as alternatives to China, with lower input costs, better demographics, and greater peace multiples due to friendlier political regimes. Finally, there continue to be strong pockets of opportunity in specific private market investments that our team continues to explore.

All that to say, the next 20 years will likely not look like the past 20 years, but there should continue to be attractive investment opportunities if assets are allocated properly.

As always, please take a look at Stephanie’s Public Market Update to gain more insight into how public markets performed in Q2 and how LotusGroup portfolios were positioned. Additionally, we welcome Sam Redman as our new Director of Alternative Assets in the Private Market Update section, as we continue to grow that program.

Cheers!

Raph & The Entire LGA Team

Public Market Update – Q2 / 2024

Stephanie Schlemeyer: Partner, Public Markets PM

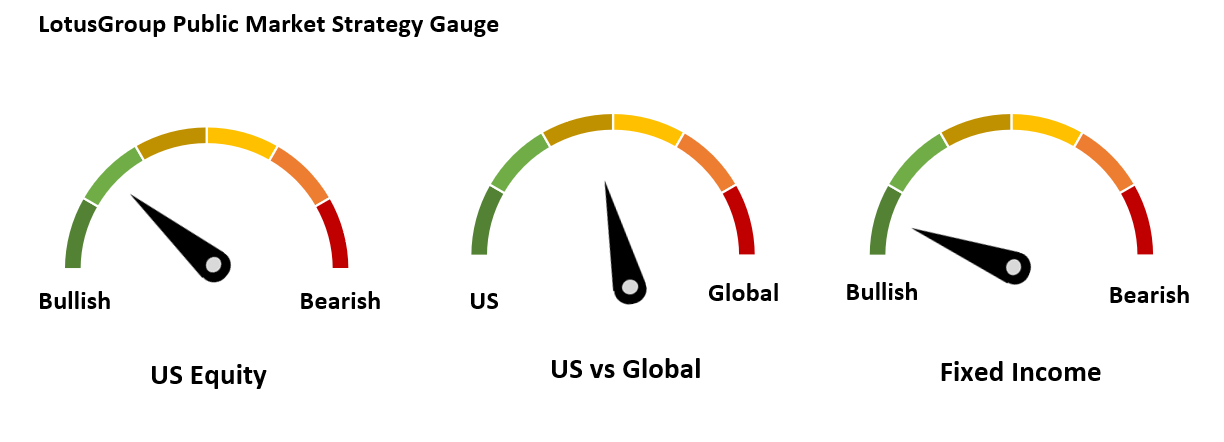

Our LGA public market strategy gauges remained unchanged during Q2 (see below):

US Equity:

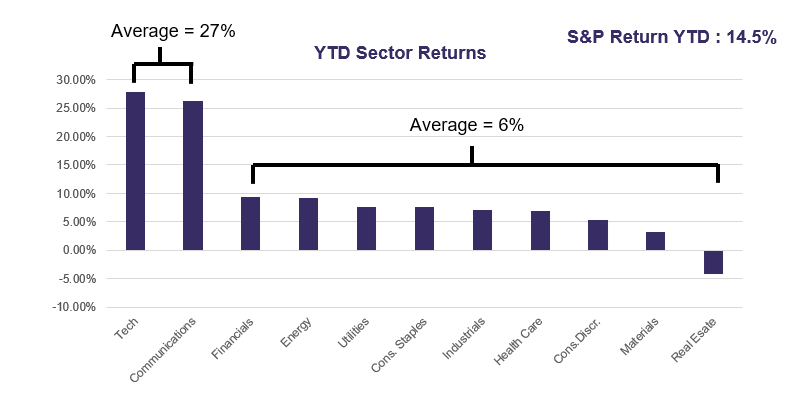

The S&P was up 3.5% this quarter, and 14.5% YTD albeit there was large dispersion amongst the various sectors that make up the index:

Q2 returns were dominated by Tech and Communications, while most other sectors were flat to negative.

Year to date, the Tech titans (Apple, Google, Amazon, etc.) have risen dramatically, while the rest of the remaining S&P Sectors are up about 6%.

Chart II – YTD S&P Sector Performance (Source: LotusGroup)

Several factors have contributed to the continued positive performance of US equities:

Strong Corporate Earnings: Many companies exceeded earnings expectations, driven by resilient consumer demand and effective cost management. The tech sector, in particular, benefited from continued digital transformation trends.

Federal Reserve Policy: The Federal Reserve maintained a cautious stance on interest rates, signaling a potential pause in rate hikes. This provided a boost to investor confidence, as lower interest rates support higher valuations for equities.

Economic Indicators: Key economic indicators such as GDP growth and unemployment rates remained favorable. The US economy showed signs of resilience, despite concerns over inflation and geopolitical tensions.

LotusGroup portfolios continued with a 75% beta positioning, generating positive returns, albeit in a slightly muted way relative to full market exposure. We will keep monitoring our indicators to determine the right time to move to 100%.

Global Equities:

Returns for Foreign Equities were positive but lagged US Equities, influenced by regional economic conditions and global events.

Emerging markets, in particular, showed signs of recovery, while developed markets had varied results.

Consequently, having an overweight in the US vs Global equities proved to be helpful during this quarter.

US Fixed income:

There were no changes to our fixed income positioning, which remained bullish with a strong preference for shorter term duration and yield maximization.

We expect to continue with the current positioning until rates begin to meaningfully decline or if there is another spike higher in inflation / rates (lower probability scenario).

Summary:

The second quarter of 2024 showcased a positive market landscape across US equity, foreign equity, and US bonds. While challenges remain, including inflation and geopolitical uncertainties, the overall market sentiment remained positive.

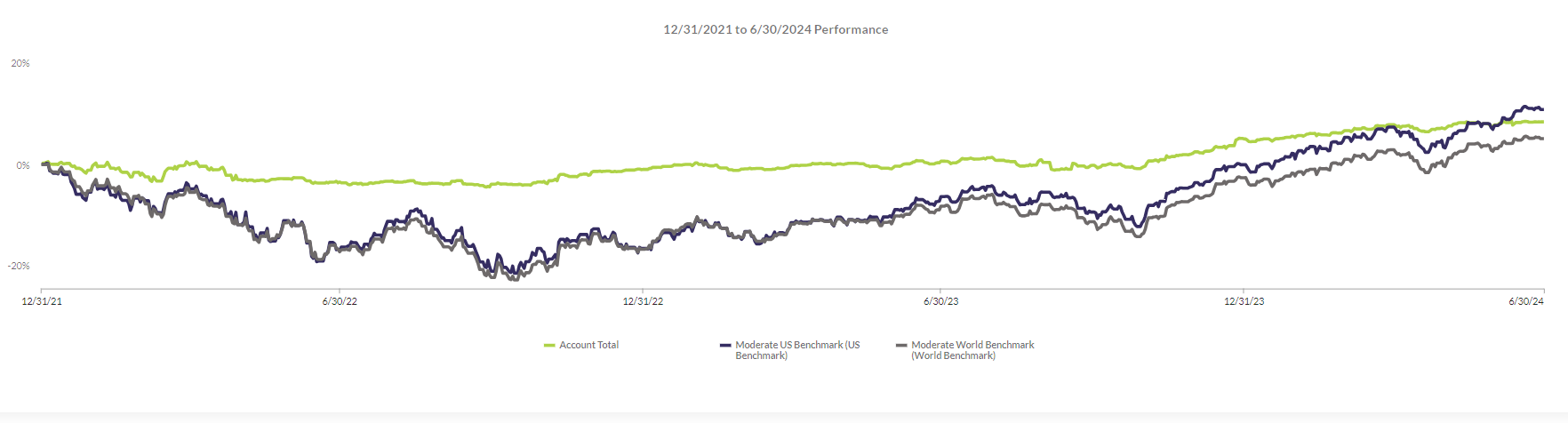

As always, we urge clients to view markets and investments with a long-term perspective and we focus portfolios on capturing the majority of market gains while minimizing volatility during major downturns. Below is an aggregate of a LotusGroup Moderate Risk Portfolio with Private, starting at the end of 2021 when the most recent market cycle began:

Chart III – LGA Tactical Moderate with Private Composite Since the Start of Most Recent Market Cycle (Source: LotusGroup)

Private Market Update – Q2/2024

Sam Redman, Director of Alternative Assets

I am pleased to begin the next chapter of my career with LotusGroup Capital. With a robust background in alternative assets and a passion for delivering exceptional results, I am eager to build on the firm’s current offerings, while infusing my own vision and experience. My aim is to build upon the already high standards and established precedent of our alternatives funds and individual investments. I look forward to working closely with our team, investment committee, and clientele in the years ahead.

LotusGroup’s private investments performed positively during 1H/2024, aligning closely with underwritten expectations. We continue to identify compelling opportunities across private markets, offering our investors avenues for growth and consistency amidst ongoing macroeconomic uncertainties. A leading bank recently characterized today’s global economic environment as “a strong economy in a fragile world.” (source: JP Morgan) With interest rates poised to remain higher for an extended period, coupled with the upcoming presidential election and increased market volatility, the demand for private uncorrelated assets remains robust.

Private Credit Opportunities

A significant focus in current markets is direct lending, or private credit. This asset class has been increasingly attractive as traditional lenders pull back from small and middle-market companies, leaving a void in available credit for a growing segment. Despite current public debt instruments offering relatively attractive interest rates compared to previous years, private credit markets can often deliver more than double the yield. We maintain a positive outlook on this space and continue to actively invest.

Manager Selection & Future Themes

Our research and due diligence efforts are heavily concentrated on manager selection across our preferred investment focus areas. The chart below, provided by Blackstone, illustrates the spread between top-tier and bottom-tier investment managers across public and private markets. This data underscores the critical importance of our private manager selection process at LotusGroup, where the performance of top-performing managers significantly outpaces their peers. Our primary focus remains on securing top-tier managers within the investment opportunities we explore.

Chart IV: The Range of Outcomes is Much wider Across Private Managers that for Public Managers (Source: Blackstone.com)

As we move through the second half of 2024, we anticipate numerous compelling opportunities for research, due diligence, and ultimately investment. As mentioned earlier, our team is particularly interested in private credit and direct lending. Additionally, we are exploring potential investments across a wide array of sectors, including aircraft leasing, distressed office space, litigation finance, and beyond.

I look forward to meeting and/or speaking with you all in the coming years and am thrilled to be part of the growing LotusGroup team.

The information contained herein, including but not limited to research, market valuations, calculations, estimates, and other material obtained from LotusGroup, and other sources, are believed to be reliable. However, LotusGroup does not warrant its accuracy or completeness. These materials are provided for informational purposes only and should not be used or construed as an offer to sell or a solicitation of an offer to buy any security. Past performance is not indicative of future results.

This blog expresses the views of the author(s) as of the date indicated, and such views are subject to change without notice. Investment advisory services are offered through LotusGroup Advisors, LLC, a federally registered investment adviser. LotusGroup transacts business only in states where it is appropriately registered, excluded, or exempted from registration requirements.The information contained within is believed to be from reliable sources. However, its accuracy, completeness, and the opinions based thereon by the author(s) are not guaranteed – no responsibility is assumed for omissions or errors. The views expressed herein reflect the authors’ judgment now, are subject to change without notice, and may or may not be updated. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must make their own evaluation and investigation of any investments considered or of any investment strategies described herein (including the risks and merits thereof), should seek professional advice for their particular circumstances, and should inform themselves as to the tax or other consequences of any investments or services considered or described herein. LotusGroup’s advisory clients will be required to execute an Investment Advisory Agreement and related Account opening documents (collectively, “Agreements”). If any of the terms or descriptions in this presentation are inconsistent with the terms of the Agreements, such Agreements shall control. Prospective investors should maintain the financial capability and willingness to accept the risks associated with any investments made, should consult the relevant investment prospectus or legal documents, and should their Advisor Representative before making investment decisions (including but not limited to an examination of the investment objectives, risks, charges, and expenses of any investment product(s) considered).

Extracted performance in this presentation is representative of a subset of investments extracted from a portfolio. Such performance is depicted in this presentation based on accounts that match the following criteria: Tactical 100 model held at Schwab with Moderate Agg risk that includes private investments. LGA employee accounts are excluded from this extracted performance. LGA will provide full performance information promptly upon request. The performance data provided herein is for information and discussion purposes only. The performance of an individual account may vary substantially based on various factors, including, but not limited to, initial account management start date, risk profiles, cash allocation, and investment restrictions, among many others. This information is unaudited. Please refer to an account’s brokerage statement for individual account information. Past performance does not guarantee future results.

To better understand the nature and scope of our advisory services and business practices, readers are encouraged to review via the SEC’s website @ www.adviserinfo.sec.gov, the adviser’s Form ADV Disclosure(s), and the Form ADV 2B Brochure Supplement of each LotusGroup Investment Professional (Click on the link, select “Investment Advisor firm,” and type in the firm name. Results will provide you both Part 1 and 2 of the LotusGroup ‘s Form ADV.).

This blog, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part in any form without our prior written consent.

US Equity:

The S&P was up 3.5% this quarter, and 14.5% YTD albeit there was large dispersion amongst the various sectors that make up the index:

US Equity:

The S&P was up 3.5% this quarter, and 14.5% YTD albeit there was large dispersion amongst the various sectors that make up the index:

Sam Redman, Director of Alternative Assets

I am pleased to begin the next chapter of my career with LotusGroup Capital. With a robust background in alternative assets and a passion for delivering exceptional results, I am eager to build on the firm’s current offerings, while infusing my own vision and experience. My aim is to build upon the already high standards and established precedent of our alternatives funds and individual investments. I look forward to working closely with our team, investment committee, and clientele in the years ahead.

LotusGroup’s private investments performed positively during 1H/2024, aligning closely with underwritten expectations. We continue to identify compelling opportunities across private markets, offering our investors avenues for growth and consistency amidst ongoing macroeconomic uncertainties. A leading bank recently characterized today’s global economic environment as “a strong economy in a fragile world.” (source: JP Morgan) With interest rates poised to remain higher for an extended period, coupled with the upcoming presidential election and increased market volatility, the demand for private uncorrelated assets remains robust.

Private Credit Opportunities

A significant focus in current markets is direct lending, or private credit. This asset class has been increasingly attractive as traditional lenders pull back from small and middle-market companies, leaving a void in available credit for a growing segment. Despite current public debt instruments offering relatively attractive interest rates compared to previous years, private credit markets can often deliver more than double the yield. We maintain a positive outlook on this space and continue to actively invest.

Manager Selection & Future Themes

Our research and due diligence efforts are heavily concentrated on manager selection across our preferred investment focus areas. The chart below, provided by Blackstone, illustrates the spread between top-tier and bottom-tier investment managers across public and private markets. This data underscores the critical importance of our private manager selection process at LotusGroup, where the performance of top-performing managers significantly outpaces their peers. Our primary focus remains on securing top-tier managers within the investment opportunities we explore.

Sam Redman, Director of Alternative Assets

I am pleased to begin the next chapter of my career with LotusGroup Capital. With a robust background in alternative assets and a passion for delivering exceptional results, I am eager to build on the firm’s current offerings, while infusing my own vision and experience. My aim is to build upon the already high standards and established precedent of our alternatives funds and individual investments. I look forward to working closely with our team, investment committee, and clientele in the years ahead.

LotusGroup’s private investments performed positively during 1H/2024, aligning closely with underwritten expectations. We continue to identify compelling opportunities across private markets, offering our investors avenues for growth and consistency amidst ongoing macroeconomic uncertainties. A leading bank recently characterized today’s global economic environment as “a strong economy in a fragile world.” (source: JP Morgan) With interest rates poised to remain higher for an extended period, coupled with the upcoming presidential election and increased market volatility, the demand for private uncorrelated assets remains robust.

Private Credit Opportunities

A significant focus in current markets is direct lending, or private credit. This asset class has been increasingly attractive as traditional lenders pull back from small and middle-market companies, leaving a void in available credit for a growing segment. Despite current public debt instruments offering relatively attractive interest rates compared to previous years, private credit markets can often deliver more than double the yield. We maintain a positive outlook on this space and continue to actively invest.

Manager Selection & Future Themes

Our research and due diligence efforts are heavily concentrated on manager selection across our preferred investment focus areas. The chart below, provided by Blackstone, illustrates the spread between top-tier and bottom-tier investment managers across public and private markets. This data underscores the critical importance of our private manager selection process at LotusGroup, where the performance of top-performing managers significantly outpaces their peers. Our primary focus remains on securing top-tier managers within the investment opportunities we explore.