Artificial Intelligence (“AI”) is all the rage these days, with positive affirmations of how it will transform a variety of industries, and negative affirmations of how it will usher in the end of humanity. While AI is the current talk of the town, it has been around for quite some time already, powering scientific breakthroughs, optimizing business performance, and permeating countless other areas around us.

So why all the current buzz?

First, engineers are starting to let computers talk to each other and make decisions that previously required human intervention. For example, rather than requiring a human to search for information and make an interpretation, AI can now search across multiple linked-up databases and provide an interpretation of such information in the form of an output. Second, a variety of leading companies have put out easy to use interfaces so the common person / public can start using these tools in an open-source manner. This open-source approach has created an immense amount of curiosity and usage, ranging from hard-core scientific and business uses, to students having computers write history papers and computer programs for them. Kidding aside, it is estimated that in coding alone, an order of magnitude of productivity improvement is right around the corner, with tech startups no longer requiring large budgets for 100s of engineers, but rather more manageable budgets with 10s of engineers and their AI sidekicks helping them to write the code. How many new ideas will be pursued with a lower startup cost requirement? Likely, this will be transformational for the tech VC community, with positive and negative repercussions.

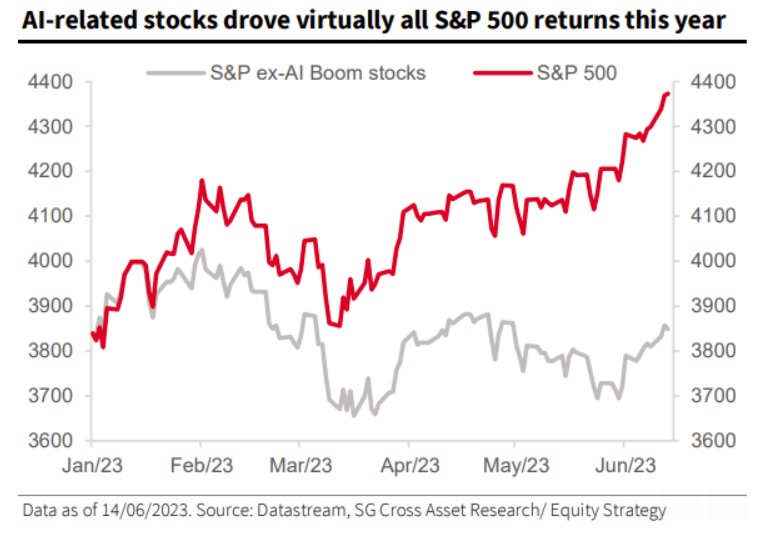

Finally, and a more cynical view, is that tech stocks were in the doldrums and needed a significant new boost of enthusiasm. As interest rates rose rapidly, many low, or no profit tech businesses experienced 50-90%+ declines or simply went out of business. The era of focusing on product growth, rapidly increasing revenues, but zero profits quickly came to a crashing end when money was no longer “free.” Investors suddenly demanded a profit, new rounds of fundraising tightened dramatically, and a massive crash occurred. With that said, AI has been a marketing bonanza for the top companies in the sector and has single-handedly pulled the S&P 500 out of its bear market (see below for the 6 month returns of the S&P 500 with and without the AI boom stocks).

As you can see, without the AI stocks in the S&P 500, the index would have posted a slightly negative return for 2023, staying in the 20%+ bear market from 2022. With that said, the question going forward will be whether this very narrow sector strength will continue to power the S&P 500 forward, whether other sectors will begin to catch up, or whether it will all peter out and restart the bear market that began in 2022.

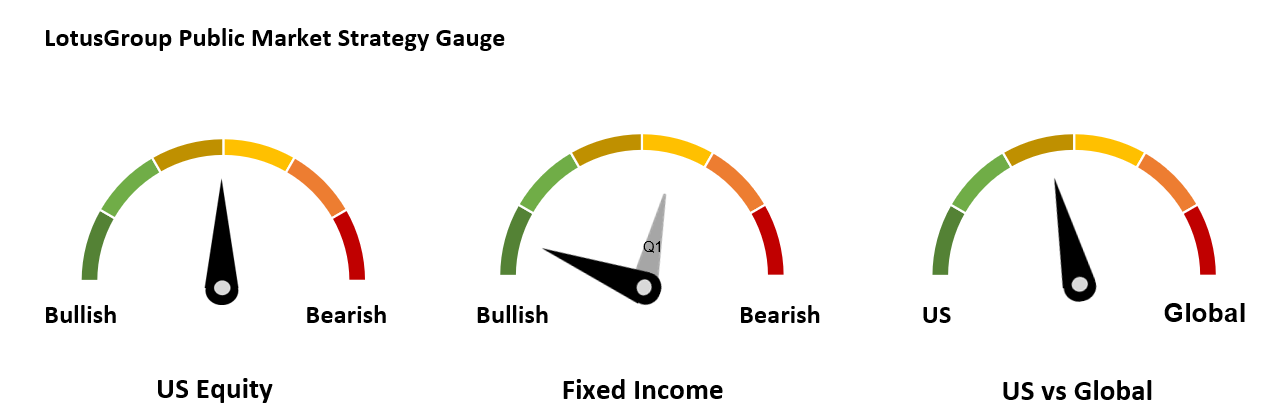

We have turned cautiously optimistic on public markets, after positioning client portfolios conservatively over the past 18-24 months of this rolling bear market. Of specific note is our move to a fully bullish position in fixed income, albeit we remain very short duration to “have our cake and eat it too.” Read more about this in Stephanie’s Public Market Update section.

We also remain very bullish on our asset-backed private alternative portfolio positions. These assets consistently delivered positive returns during the difficult bear market of 2022 and earlier during the COVID-19 market scare of 1H/2020. Read more about the upcoming launch of our 3rd diversified fund as well as an interesting case study of an attractive recent deal in Louis’ Private Market Update section.

Wishing everyone a wonderful summer!

Cheers Raph & The Entire LGA Team

Public Market Update – Q2/2023

Stephanie Schlemeyer: Partner & Public Markets PM

US Equity: S&P 500 returns continued to rebound during Q2, boosted by a surge in a small group of familiar tech companies (Google, Microsoft, Amazon, Apple, etc.). While the bounce higher has been impressive, in most cases these stocks have yet to recover from their previous highs 18-24 months ago, while experiencing volatility of 30%, 50% and even 80% drawdowns along the way.

More specifically, the near-term bounce has been driven by tech stocks that are focused in the Artificial Intelligence (“AI”) sector. There are many other previously popular growth and tech stocks that have not seen the same recovery and remain down meaningfully (Peloton still down 95% from peaks, Zoom still down 85% from its peak, etc.).

LotusGroup portfolios have been positioned in a neutral weight to US equities, participating in the market with a 50% beta positioning. As a reminder, “beta” represents the approximate relative return to a benchmark, so a “50% beta” would be the equivalent of experiencing half of the upside and half the downside of a specific benchmark.

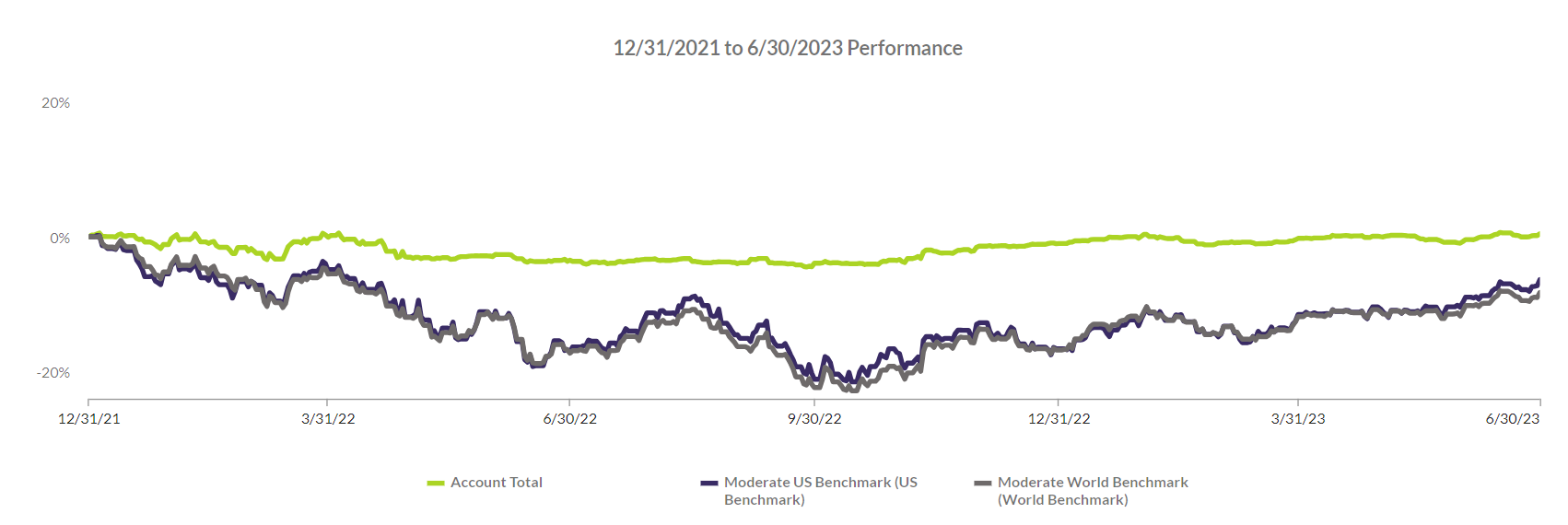

For perspective, the chart below shows our green composite results relative to benchmarks since the bear market began in late 2021 (using our avg Tactical portfolio with a Moderate risk profile and an allocation to Private Investments). While our initial focus was on protecting portfolios against the downturn, we have more recently turned towards partially participating in the recovery.

Chart I – LGA Tactical Moderate with Private Composite 1H/2023 (Source: LotusGroup)

The jury is still out on whether a renewed bear market will materialize (perhaps driven by far tighter financial conditions) or whether we have skirted a recession and begun a new bull market.

We will continue to monitor the markets and our models and make necessary adjustments to portfolio beta.

Fixed Income We have moved the fixed income dial from neutral to bullish this quarter. For clarification, we are not bullish on all fixed income, for example we still think there is risk in longer duration securities. However, short duration fixed income assets are now far superior in their risk/return characteristics relative to liquid fixed income alternative positions. While liquid alts like “merger arbitrage” and “managed futures” served us well over the past 5 years, and helped portfolios almost completely avoid the fixed income carnage in 2022, we have now moved fully into short-term treasuries and other fixed income. Specifically, LotusGroup portfolios are currently allocated to core fixed income, some strategic fixed income, short-term treasuries and short-term corporates.

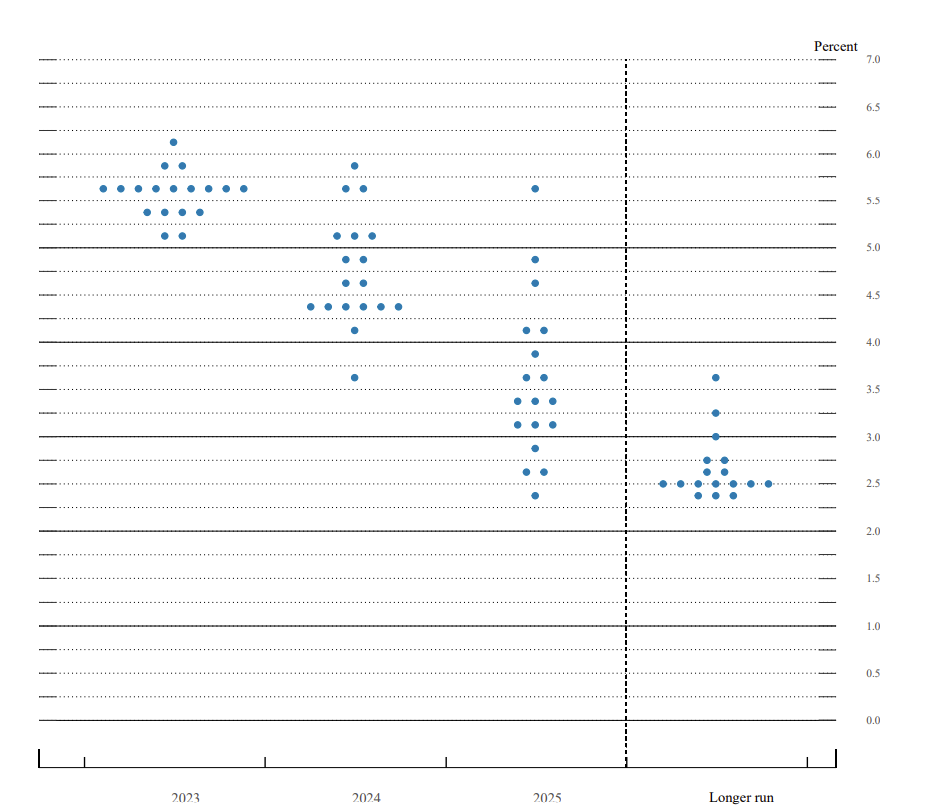

In market news, after 10 consecutive rate hikes, the Fed finally rested this quarter, leaving rates unchanged. Projections as of today are that two more rate hikes are on their way. See below for the most recent dot plot from the June 2023 meeting:

Chart II – FOMC participants’ assessments of appropriate monetary policy (Source: FederalReserve.Gov)

What does this mean for your portfolio?

We remain focused on shorter duration assets, which in today’s market allow us to “have our cake and eat it to.” With an inverted yield curve, short duration assets are paying out the highest yields along the curve. Additionally, since short-term securities self-liquidate very quickly, they don’t participate in value declines like longer duration assets do if rates continue to rise. So, for the time being, being in short-duration fixed income is the place to be, generating maximum yields and protecting against price depreciation.

Global Equities We ended the quarter as we began, with a small tilt toward US equities vs Global equities. This positioning has proven to be correct as US equities have produced approximately double the return of global equities year-to-date.

As mentioned above, we remain cautiously optimistic and will continue to diligently monitor our models and the markets, with a goal of allocating in a disciplined manner to meet each investor’s unique set of portfolio goals.

Private Market Update – Q2/2023

Louis Frank: Partner, Private Market PM

Our private market pipeline is as robust as ever, and we are sourcing several attractive risk-adjusted opportunities.

Last quarter we touched on the growing opportunity within the “specialty finance” area. This space continues to grow as regional banks tighten credit standards, and many small businesses struggle with liquidity issues. With banks out of the picture and demand for alternative financing growing, specialty lenders can charge “take it or leave it” financing terms.

We have consistently seen rates in the mid-teens, very secure 30-60% LTVs (loan-to-value), senior preference rights, and strong personal guarantees. This dynamic has created above equity-like returns in the specialty lending space, and we continue to selectively fill our pipeline with partners we trust.

Below is an example deal in this specialty lending space.

Investment Highlights:

Senior Secured Loan Collateralzied by three pieces of real estate

$100MM+ Personal Gurantor

40% Loan-to-Value (60% 1st loss equity in front of our position)

4% Origination Fee

12% Annualized Cash Pay

Investment Overview: A UHNW individual was looking to make a solar tax credit investment and was willing to collateralize personal residences to receive funding. He chose to work with our sponsor due to a lack of bank funding and our sponsor’s ability to close quickly.

Investment Structure: This was structured as a co-investment with zero fees to LotusGroup. We have collateralized stakes in all three of the pledged properties and a personal guarantee from the borrower. The borrower will have 12 months to repay the principal with the option to extend 90 days twice. The borrower would pay a 1% extension fee per each extension option.

The information contained herein, including but not limited to research, market valuations, calculations, estimates, and other material obtained from LotusGroup, and other sources, are believed to be reliable. However, LotusGroup does not warrant its accuracy or completeness. These materials are provided for informational purposes only and should not be used or construed as an offer to sell or a solicitation of an offer to buy any security. Past performance is not indicative of future results.

This blog expresses the views of the author(s) as of the date indicated, and such views are subject to change without notice. Investment advisory services are offered through LotusGroup Advisors, LLC, a federally registered investment adviser. LotusGroup transacts business only in states where it is appropriately registered, excluded, or exempted from registration requirements.The information contained within is believed to be from reliable sources. However, its accuracy, completeness, and the opinions based thereon by the author(s) are not guaranteed – no responsibility is assumed for omissions or errors. The views expressed herein reflect the authors’ judgment now, are subject to change without notice, and may or may not be updated. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must make their own evaluation and investigation of any investments considered or of any investment strategies described herein (including the risks and merits thereof), should seek professional advice for their particular circumstances, and should inform themselves as to the tax or other consequences of any investments or services considered or described herein. LotusGroup’s advisory clients will be required to execute an Investment Advisory Agreement and related Account opening documents (collectively, “Agreements”). If any of the terms or descriptions in this presentation are inconsistent with the terms of the Agreements, such Agreements shall control. Prospective investors should maintain the financial capability and willingness to accept the risks associated with any investments made, should consult the relevant investment prospectus or legal documents, and should their Advisor Representative before making investment decisions (including but not limited to an examination of the investment objectives, risks, charges, and expenses of any investment product(s) considered).

Extracted performance in this presentation is representative of a subset of investments extracted from a portfolio. Such performance is depicted in this presentation based on accounts that match the following criteria: Tactical 100 model held at TD Ameritrade with Moderate Agg risk that includes private investments. LGA employee accounts are excluded from this extracted performance. LGA will provide full performance information promptly upon request. The performance data provided herein is for information and discussion purposes only. The performance of an individual account may vary substantially based on various factors, including, but not limited to, initial account management start date, risk profiles, cash allocation, and investment restrictions, among many others. This information is unaudited. Please refer to an account’s brokerage statement for individual account information. Past performance does not guarantee future results.

To better understand the nature and scope of our advisory services and business practices, readers are encouraged to review via the SEC’s website @ www.adviserinfo.sec.gov, the adviser’s Form ADV Disclosure(s), and the Form ADV 2B Brochure Supplement of each LotusGroup Investment Professional (Click on the link, select “Investment Advisor firm,” and type in the firm name. Results will provide you both Part 1 and 2 of the LotusGroup ‘s Form ADV.).

This blog, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part in any form without our prior written consent.

As you can see, without the AI stocks in the S&P 500, the index would have posted a slightly negative return for 2023, staying in the 20%+ bear market from 2022. With that said, the question going forward will be whether this very narrow sector strength will continue to power the S&P 500 forward, whether other sectors will begin to catch up, or whether it will all peter out and restart the bear market that began in 2022.

We have turned cautiously optimistic on public markets, after positioning client portfolios conservatively over the past 18-24 months of this rolling bear market. Of specific note is our move to a fully bullish position in fixed income, albeit we remain very short duration to “have our cake and eat it too.” Read more about this in Stephanie’s Public Market Update section.

We also remain very bullish on our asset-backed private alternative portfolio positions. These assets consistently delivered positive returns during the difficult bear market of 2022 and earlier during the COVID-19 market scare of 1H/2020. Read more about the upcoming launch of our 3rd diversified fund as well as an interesting case study of an attractive recent deal in Louis’ Private Market Update section.

Wishing everyone a wonderful summer!

Cheers Raph & The Entire LGA Team

As you can see, without the AI stocks in the S&P 500, the index would have posted a slightly negative return for 2023, staying in the 20%+ bear market from 2022. With that said, the question going forward will be whether this very narrow sector strength will continue to power the S&P 500 forward, whether other sectors will begin to catch up, or whether it will all peter out and restart the bear market that began in 2022.

We have turned cautiously optimistic on public markets, after positioning client portfolios conservatively over the past 18-24 months of this rolling bear market. Of specific note is our move to a fully bullish position in fixed income, albeit we remain very short duration to “have our cake and eat it too.” Read more about this in Stephanie’s Public Market Update section.

We also remain very bullish on our asset-backed private alternative portfolio positions. These assets consistently delivered positive returns during the difficult bear market of 2022 and earlier during the COVID-19 market scare of 1H/2020. Read more about the upcoming launch of our 3rd diversified fund as well as an interesting case study of an attractive recent deal in Louis’ Private Market Update section.

Wishing everyone a wonderful summer!

Cheers Raph & The Entire LGA Team

US Equity: S&P 500 returns continued to rebound during Q2, boosted by a surge in a small group of familiar tech companies (Google, Microsoft, Amazon, Apple, etc.). While the bounce higher has been impressive, in most cases these stocks have yet to recover from their previous highs 18-24 months ago, while experiencing volatility of 30%, 50% and even 80% drawdowns along the way.

More specifically, the near-term bounce has been driven by tech stocks that are focused in the Artificial Intelligence (“AI”) sector. There are many other previously popular growth and tech stocks that have not seen the same recovery and remain down meaningfully (Peloton still down 95% from peaks, Zoom still down 85% from its peak, etc.).

LotusGroup portfolios have been positioned in a neutral weight to US equities, participating in the market with a 50% beta positioning. As a reminder, “beta” represents the approximate relative return to a benchmark, so a “50% beta” would be the equivalent of experiencing half of the upside and half the downside of a specific benchmark.

For perspective, the chart below shows our green composite results relative to benchmarks since the bear market began in late 2021 (using our avg Tactical portfolio with a Moderate risk profile and an allocation to Private Investments). While our initial focus was on protecting portfolios against the downturn, we have more recently turned towards partially participating in the recovery.

US Equity: S&P 500 returns continued to rebound during Q2, boosted by a surge in a small group of familiar tech companies (Google, Microsoft, Amazon, Apple, etc.). While the bounce higher has been impressive, in most cases these stocks have yet to recover from their previous highs 18-24 months ago, while experiencing volatility of 30%, 50% and even 80% drawdowns along the way.

More specifically, the near-term bounce has been driven by tech stocks that are focused in the Artificial Intelligence (“AI”) sector. There are many other previously popular growth and tech stocks that have not seen the same recovery and remain down meaningfully (Peloton still down 95% from peaks, Zoom still down 85% from its peak, etc.).

LotusGroup portfolios have been positioned in a neutral weight to US equities, participating in the market with a 50% beta positioning. As a reminder, “beta” represents the approximate relative return to a benchmark, so a “50% beta” would be the equivalent of experiencing half of the upside and half the downside of a specific benchmark.

For perspective, the chart below shows our green composite results relative to benchmarks since the bear market began in late 2021 (using our avg Tactical portfolio with a Moderate risk profile and an allocation to Private Investments). While our initial focus was on protecting portfolios against the downturn, we have more recently turned towards partially participating in the recovery.

Our private market pipeline is as robust as ever, and we are sourcing several attractive risk-adjusted opportunities.

Last quarter we touched on the growing opportunity within the “specialty finance” area. This space continues to grow as regional banks tighten credit standards, and many small businesses struggle with liquidity issues. With banks out of the picture and demand for alternative financing growing, specialty lenders can charge “take it or leave it” financing terms.

We have consistently seen rates in the mid-teens, very secure 30-60% LTVs (loan-to-value), senior preference rights, and strong personal guarantees. This dynamic has created above equity-like returns in the specialty lending space, and we continue to selectively fill our pipeline with partners we trust.

Below is an example deal in this specialty lending space.

Investment Highlights:

Our private market pipeline is as robust as ever, and we are sourcing several attractive risk-adjusted opportunities.

Last quarter we touched on the growing opportunity within the “specialty finance” area. This space continues to grow as regional banks tighten credit standards, and many small businesses struggle with liquidity issues. With banks out of the picture and demand for alternative financing growing, specialty lenders can charge “take it or leave it” financing terms.

We have consistently seen rates in the mid-teens, very secure 30-60% LTVs (loan-to-value), senior preference rights, and strong personal guarantees. This dynamic has created above equity-like returns in the specialty lending space, and we continue to selectively fill our pipeline with partners we trust.

Below is an example deal in this specialty lending space.

Investment Highlights: