Large rises in interest rates typically drive major economic shifts, albeit they can take time to fully affect the status quo. A lag effect tends to occur as investors are remiss in letting go of previously high-returning asset classes. Additionally, investors are often slow to recognize which new winners will emerge from the sea change. With a Fed Funds rate now 5%+ higher than it was just a little over a year ago, the effects are starting to take hold.

For example, small-to-mid-sized tech companies with no or low profit have had meteoric declines after many years of attractive returns. Long-term fixed income was also hammered as rising rates caused a major revaluation of 10, 20, and 30yr bonds that were fixed to low rates. Finally, the “always goes up” real estate sector saw declines, first in the commercial office space, and now in a broader swath of sectors, including residential homes (see declining values on Zillow).

As you take a read through Stephanie’s Public Market Update, we remind you of our conservative positioning over the past couple years to avoid these downtrends. While hindsight is 20/20, as of a couple years ago, there were massive cheerleaders for all of these “hot” investment areas.

On the positive side, opportunities have emerged in multiple areas. Public short-duration fixed income is now paying over 5%, the highest rate we have seen in over a decade (16 years to be exact)! Additionally, private credit and real estate senior debt are presenting as double-digit return opportunities. Please read through Louis’ Private Market Update to learn more about the opportunities we are aggressively pursuing with our qualified and accredited clientele.

During major bull markets, many want to keep chasing after the fastest growing ideas…which can work for a while, but often end in tears. However, during longer-term bear markets, many want to batten down the hatches and sit in cash. Today’s 4%+ CD and money market environment strongly calls to that mindset.

To some extent, we agree with having an allocation to high-yielding cash until the “new bull market” versus “continued bear market” debate is further resolved. However, too large of a cash allocation risks a high tax bill, as CDs, money markets and Treasuries are taxed at the highest income tax rate.

For now, we will continue to be slightly cautious in public equity markets, take advantage of higher 5%+ fixed income rates on a growing allocation, and aggressively pursue double-digit return opportunities in the private credit and specialty finance spaces through our private diversified funds.

We wish you all a fantastic autumn and hope you get some time to enjoy and reflect with your family in the holiday season ahead.

Cheers Raph & The Entire LGA Team

Public Market Update – Q3/2023

Stephanie Schlemeyer: Partner & Public Markets PM

US Equity:

The US Equity market had a weak third quarter, marked by declining stock prices and subdued investor confidence.

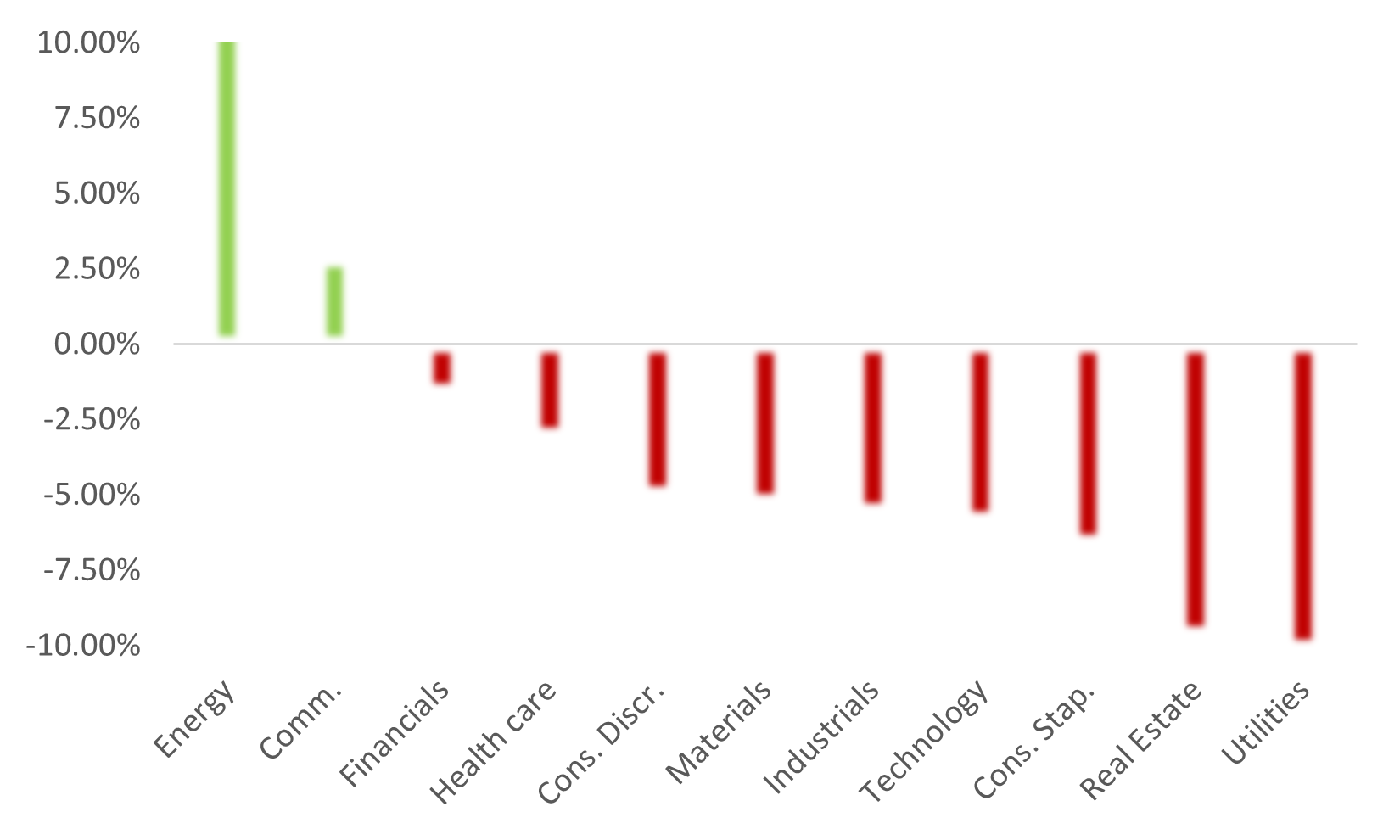

9 out of the 11 market sectors were negative this quarter.

Chart I – US Equity Asset Class Performance Q3/2023 (Source: LotusGroup)

LotusGroup portfolios entered the quarter with reduced exposure to these markets, resulting in lower volatility.

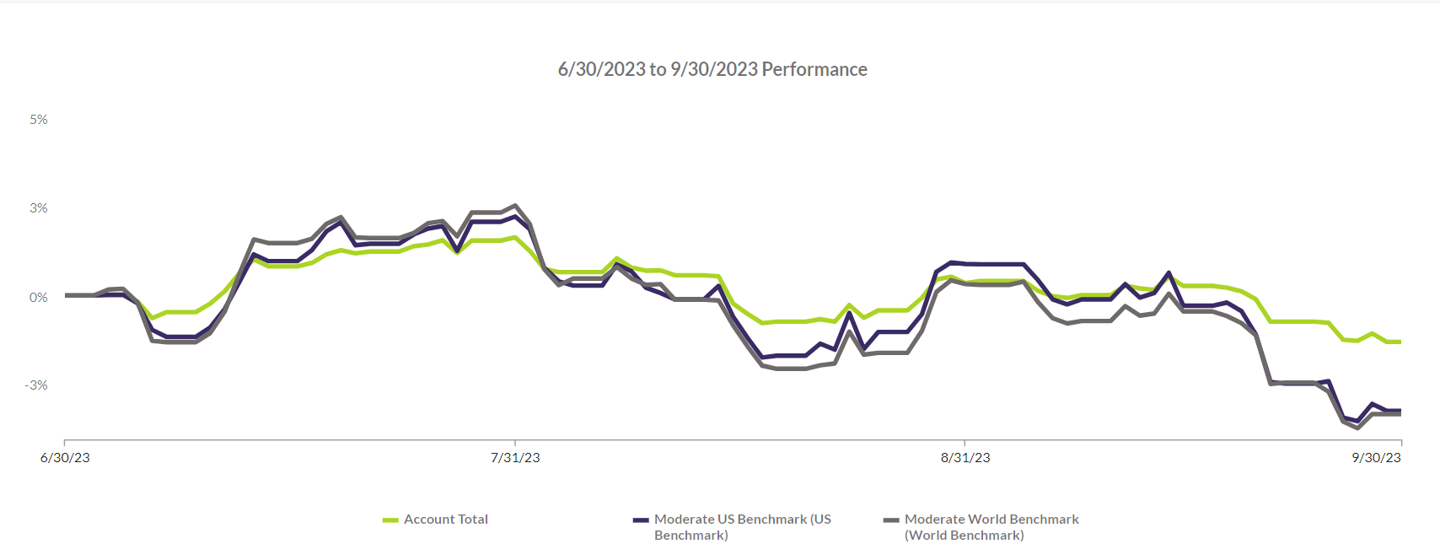

Q3 returns for a typical LotusGroup tactical public + private portfolio is illustrated below (green line), as compared to the global benchmark (gray) & US market benchmark (purple).

This chart illustrates the generally lower volatility of LotusGroup portfolios throughout Q3, as well as a slightly smaller decline relative to benchmarks.

Chart II – LGA Tactical Moderate with Private Composite 13/2023 (Source: LotusGroup)

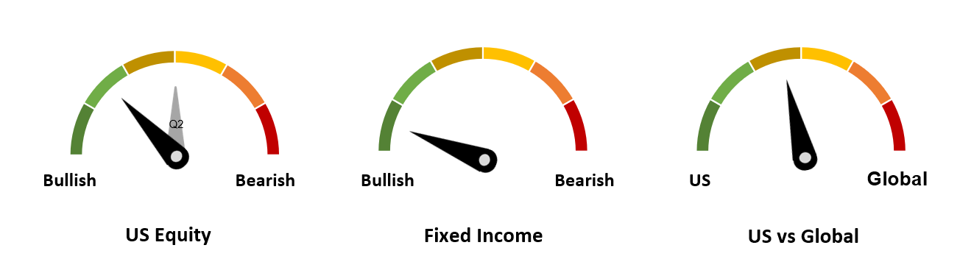

The above notwithstanding, we slightly increased our US allocation towards the end of the quarter, as technicals improved and sentiment cooled off.

This increase moved our current US equity allocation from neutral, to moderately-bullish.

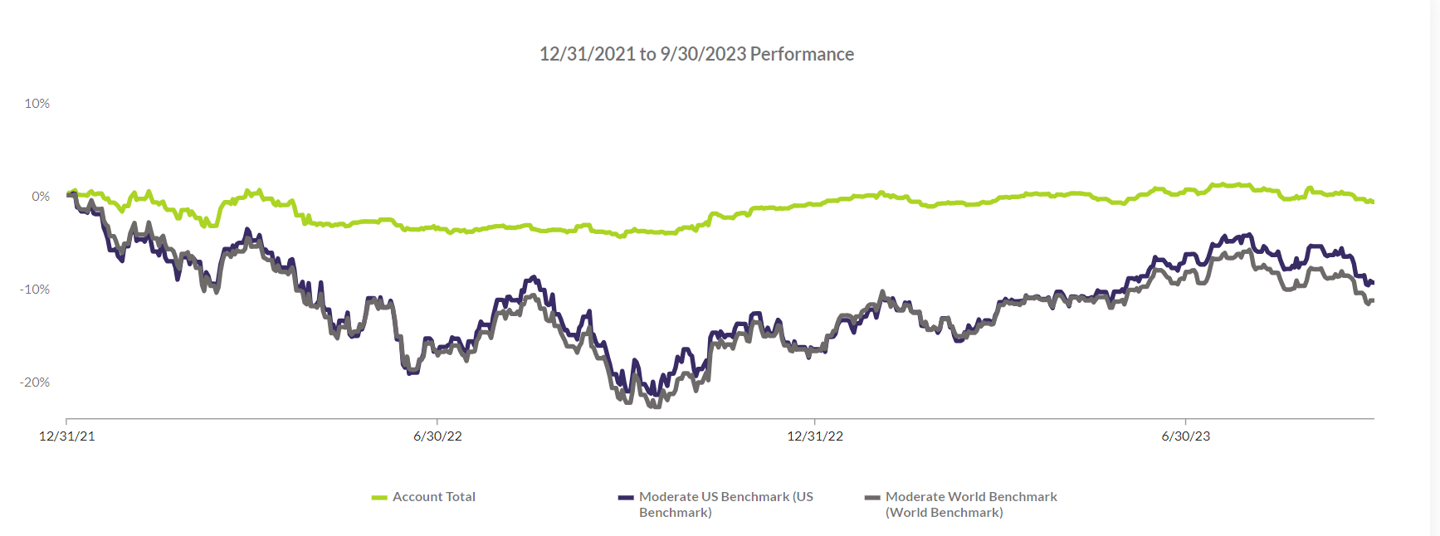

Looking back since late 2021, we had been protecting portfolios against the downturn, while more recently have been increasing our exposure as a potential new bull market emerges.

Chart III – LGA Tactical Moderate with Private Composite YTD 2023 (Source: LotusGroup)

We will continue to monitor our market indicators to help determine whether we are in a renewed bull market or if the early 2023 gains were just a bounce within a longer-term downtrend.

As the evidence unfolds, we will look to either go all in with a 100% bullish position or reduce exposure once again for protection.

Fixed Income

We ended Q3 as we began, with a bullish view on short-duration US fixed income and money market instruments.

LotusGroup portfolios included positions now yielding 5%+ for the first time in a decade!

Simultaneously, long-term fixed income suffered its worst quarter on record, as rapidly rising rates contributed to declining values.

Positively, LotusGroup’s short-duration positioning helped client portfolios to miss most if not all of these declines.

Global Equities

We continued to favor US vs global in LotusGroup portfolios.

This once again proved helpful, with both foreign developed and emerging markets underperforming the US for Q3.

Private Market Update – Q3/2023

Louis Frank: Partner, Private Market PM

Our private market pipeline continues to be robust, with multiple attractive risk-adjusted opportunities in the pipeline.

As higher rates, stricter credit parameters, and reduced liquidity sets into the market, our deal pipeline seems to grow weekly.

We remain extremely selective regarding deal quality and focus on partners with best-in-class track records.

With the launch of our 3rd diversified fund in July, we are actively raising and deploying capital to take advantage of our deal pipeline.

We believe that the next 24-36 months should provide returns in certain asset classes that we have not seen in nearly a decade.

Below is an example deal that we recently sourced through a preferred partnership of ours:

Investment Highlights:

Investment into a diversified portfolio of high-profile patient infringement cases

Cases are sourced by a leading litigation finance originator

Target IRRS of 25%+

The downside is capped due to an insurance policy on investment principal.

Investment Overview: The program works on behalf of patent owners and investors, with defendants including well-capitalized technology giants. These cases are sourced and structured by a reputable litigation finance originator, further diligence by lead investors, and vetted with scrutiny by the insurance carriers. The potential for substantial settlements and damages along with capped losses through insurance coverage, creates a compelling risk/return profile.

Investment Structure: This was structured as a co-investment with reduced fees to LotusGroup investors. The opportunity is structured such that the investment vehicle pays a portion of case legal fees & expenses on behalf of the patent owner as plaintiff, with the vehicle receiving a percentage of the damages or settlement proceeds from the case. Our downside is capped to 87% of the investment principal value as the vehicle has an insurance wrapper.

The information contained herein, including but not limited to research, market valuations, calculations, estimates, and other material obtained from LotusGroup, and other sources, are believed to be reliable. However, LotusGroup does not warrant its accuracy or completeness. These materials are provided for informational purposes only and should not be used or construed as an offer to sell or a solicitation of an offer to buy any security. Past performance is not indicative of future results.

This blog expresses the views of the author(s) as of the date indicated, and such views are subject to change without notice. Investment advisory services are offered through LotusGroup Advisors, LLC, a federally registered investment adviser. LotusGroup transacts business only in states where it is appropriately registered, excluded, or exempted from registration requirements.The information contained within is believed to be from reliable sources. However, its accuracy, completeness, and the opinions based thereon by the author(s) are not guaranteed – no responsibility is assumed for omissions or errors. The views expressed herein reflect the authors’ judgment now, are subject to change without notice, and may or may not be updated. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must make their own evaluation and investigation of any investments considered or of any investment strategies described herein (including the risks and merits thereof), should seek professional advice for their particular circumstances, and should inform themselves as to the tax or other consequences of any investments or services considered or described herein. LotusGroup’s advisory clients will be required to execute an Investment Advisory Agreement and related Account opening documents (collectively, “Agreements”). If any of the terms or descriptions in this presentation are inconsistent with the terms of the Agreements, such Agreements shall control. Prospective investors should maintain the financial capability and willingness to accept the risks associated with any investments made, should consult the relevant investment prospectus or legal documents, and should their Advisor Representative before making investment decisions (including but not limited to an examination of the investment objectives, risks, charges, and expenses of any investment product(s) considered).

Extracted performance in this presentation is representative of a subset of investments extracted from a portfolio. Such performance is depicted in this presentation based on accounts that match the following criteria: Tactical 100 model held at TD Ameritrade with Moderate Agg risk that includes private investments. LGA employee accounts are excluded from this extracted performance. LGA will provide full performance information promptly upon request. The performance data provided herein is for information and discussion purposes only. The performance of an individual account may vary substantially based on various factors, including, but not limited to, initial account management start date, risk profiles, cash allocation, and investment restrictions, among many others. This information is unaudited. Please refer to an account’s brokerage statement for individual account information. Past performance does not guarantee future results.

To better understand the nature and scope of our advisory services and business practices, readers are encouraged to review via the SEC’s website @ www.adviserinfo.sec.gov, the adviser’s Form ADV Disclosure(s), and the Form ADV 2B Brochure Supplement of each LotusGroup Investment Professional (Click on the link, select “Investment Advisor firm,” and type in the firm name. Results will provide you both Part 1 and 2 of the LotusGroup ‘s Form ADV.).

This blog, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part in any form without our prior written consent.

US Equity:

The US Equity market had a weak third quarter, marked by declining stock prices and subdued investor confidence.

9 out of the 11 market sectors were negative this quarter.

US Equity:

The US Equity market had a weak third quarter, marked by declining stock prices and subdued investor confidence.

9 out of the 11 market sectors were negative this quarter.