Managing investment strategies for our diverse clientele is an enjoyable and meaningful job for our entire team here at LotusGroup. Our advisors continuously assess financial plans, manage client emotions, and behaviorally advise on appropriate investment strategies.

Meanwhile, our investment teams are constantly evaluating the macro landscape, monitoring our investment indicators, and building potential scenarios that we see ahead. Rather than getting fixated on a single forecast, we stress test different possibilities to position portfolios accordingly.

Here are a few areas we are reviewing today:

US equity valuations indicate a reasonably high likelihood of either muted returns in the decade ahead or a one-time major market sell-off.

Global equity valuations seem to indicate a reversal from US outperformance to global outperformance in the mid-term future, with the catalyst for such event currently TBD.

Fixed income has resurfaced as an investable asset class in the 5%+ yielding range, after nearly a decade of very low returns.

High-flier private alts in the venture capital, private equity and real estate equity areas have been suffering from higher rates.

LGA-type private alts in the specialty finance and credit spaces have been benefiting from higher rates.

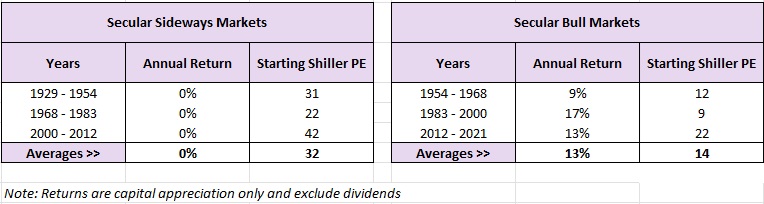

Providing additional detail to the first bullet point above, 2021-2023 could possibly be the start of a decade of muted returns. This type of scenario has occurred three other times over the past ~100 years as seen on the left-hand side of the chart below, before giving way to strong secular bull markets illustrated on the right side:

Secular Market Returns and Starting Valuation Metric Shiller PE from 1929 – 2021

For the sideways scenarios with a 0% return, they started from an average Shiller PE valuation level = 32. Considering this metric was 38 in late 2021, there is a strong possibility that we could be facing a decade of muted returns ahead while valuations come back down to earth (“The Pause that Refreshes”). This metric has declined from 38 to the current level of 32 over the past two years, while equity market returns were 0% (down in 2022 with 2023 rebound back to the same level they started 24 months ago) …so it is possible that this process of refreshing has already begun.

There are lower probability scenarios we are reviewing as well, but we wanted to at least highlight one strong possibility and the underlying data that goes into our forecasting. We will also save for another time all the details we review for each of the other high-level areas I mentioned earlier in this post (global equity, fixed income, private alts, etc).

For now, take a read through Stephanie’s Public Market Update to see additional detail on the 2021-2023 public investment markets and how we performed. Additionally, take a peek at Louis’ Private Market Update to learn more about the private investment sectors we are avoiding and where we are pressing our bets. Louis also includes an interesting example of a recently sourced deal that we believe is in the sweet spot for today’s sideways and higher interest rate environment.

We hope you all had a great holiday season and have started off the New Year with gusto. It’s a great time to be alive and pursuing our interests in life (sure beats the alternative)!

Cheers Raph & The Entire LGA Team

Public Market Update – Q4/2023, FY/2023, and Two-Year Results

Stephanie Schlemeyer: Partner & Public Markets PM

US Equity:

We ended Q4 as we began with portfolios positioned moderately bullish (75% beta to market), albeit with a couple months mid-quarter in a fully bullish position (100% beta to the market).

We’ll first look at how the market performed in 2023 and then review how we were positioned throughout the year.

The US stock market had a strong performance in 2023.

The performance across the different sectors varied greatly: some sectors had very strong performance (tech), some flat (energy), and some negative (utilities). The return dispersion from the highest return (tech) to the lowest (utilities) was above average compared to years past.

The below chart shows the S&P’s (light pink line) overall performance was mainly driven by a few sectors.

Chart I – US Equity Asset Class Performance Q4/2023 (Source: LotusGroup)

Around midyear, the market increase was driven by only a few mega cap tech stocks, illustrated by an average 16% market return (S&P 500 returns) while the median return was only 3.8%. This phenomenon in investment terms is called having unhealthy “breadth,” meaning that the returns were driven by very few sectors, instead of a healthier scenario where many sectors drive the returns. By year end, breadth improved moderately, but the median return was still only half of S&P 500 average returns.

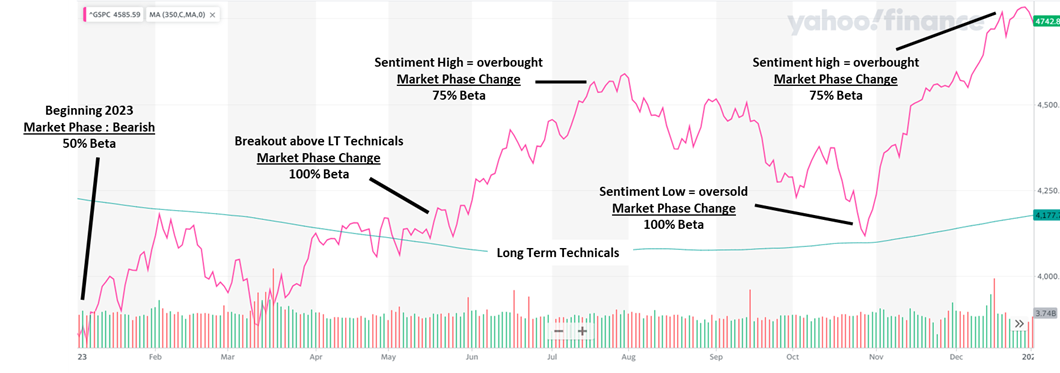

Now that we’ve looked at how the S&P 500 and its various sectors performed throughout 2023, let’s review how your LGA portfolios were positioned:

Chart II – LotusGroup Tactical Portfolio Adjustments During Year 2023

Client portfolios began the year with a 50% beta to markets given our continued focus on asset protection after the 2022 major declines. In Q2, our investment indicators confirmed the end of the previous bear market, and we moved portfolios to a fully bullish 100% beta position. Thereafter, we made three different changes to moderately decrease, increase, and again decrease market exposure as illustrated in Chart II above. Each specific move helped add to 2H/2023 relative outperformance to benchmarks.

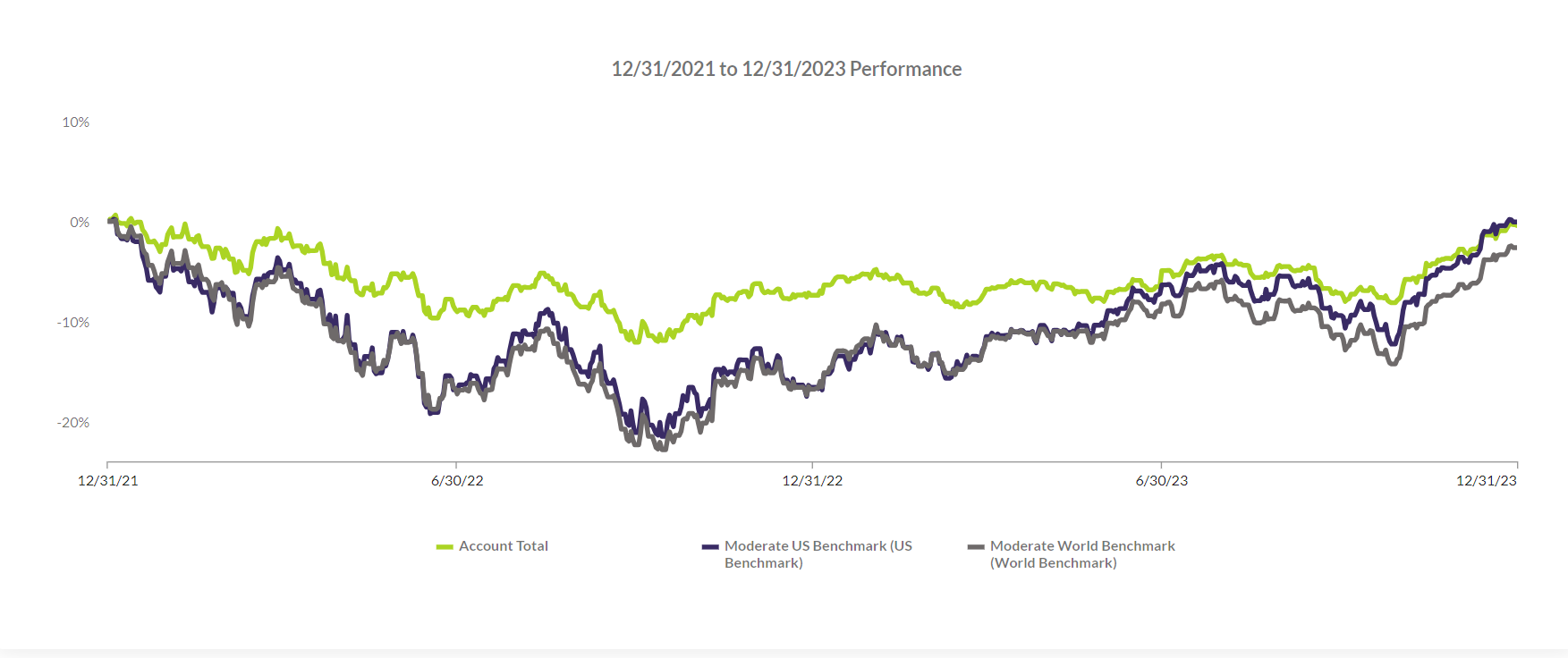

When we put the previous two years together (bear market in 2022 and bull rebound in 2023), we can see how our models perform over time vs focusing on a single quarter or year’s return. Please see Chart III below for an example of our “Tactical Strategy – Moderate with Private Allocation” portfolio (the green line is client performance and other lines are benchmarks). You can see a muted decline during the bear market of 2022 when we protected portfolios and then a subsequent participation in the 2023 rebound for a net-net outperformance relative to benchmarks.

Chart III – LGA Tactical Moderate with Private Composite 2024 (Source: LotusGroup)

Our goal with clients in the “Global Strategy – Moderate with Private Allocation” is to participate more heavily in markets but to dampen volatility during downturns. Chart IV below illustrates how this worked over the past two years, with a similar market return to benchmarks along with a lower drawdown during the bear market of 2022 (same returns + lower volatility).

Chart IV- LGA Global Moderate with Private Composite 2024(Source: LotusGroup)

Looking forward, we envision a few scenarios:

Scenario 1 (highest likelihood): The market continues to chop sideways, and we adjust portfolio exposures up (75-100% beta) and down (0-50% beta) according to our models.

Scenario 2 (possible): Equity markets breakout to new bullish highs and we participate at 75% beta while 25% of our allocation remains in treasuries yielding 5%+ right now.

Scenario 3 (possible): A major bear market appears; in which case we will once again protect portfolios with 0-50% beta positioning based on the client’s chosen strategy.

Global Equities

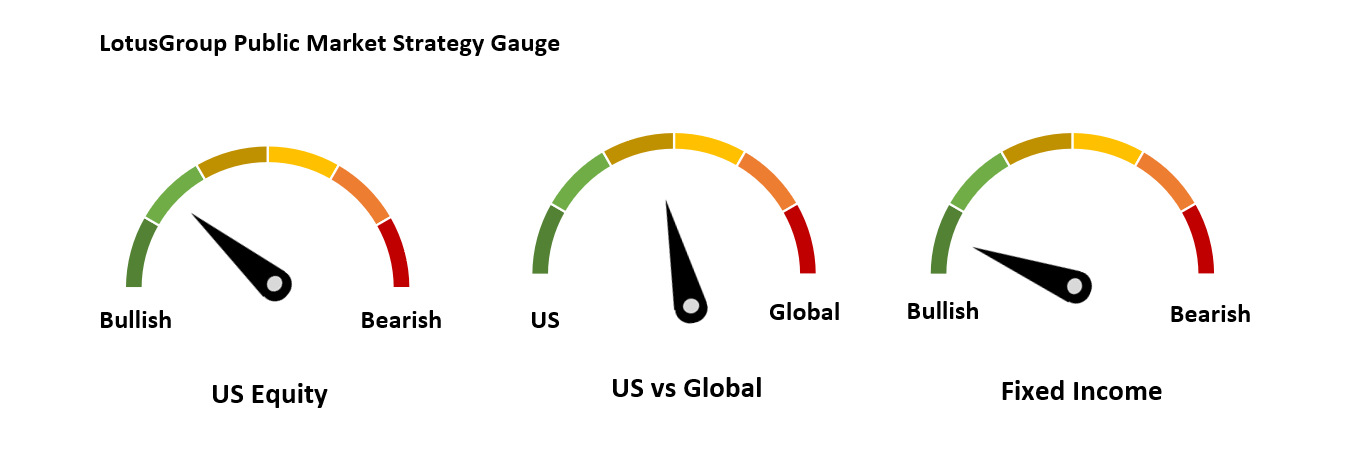

We remain overweight US equities vs Global equities. This overweight proved to be helpful for 2023 relative to global benchmarks as the US once again outperformed. On an absolute basis, even having a small foreign exposure (vs only US) added some drag 2023 performance. We continue to monitor this very long-in-the-tooth dynamic for a reversal in the years ahead, especially given much lower valuations outside the US and long-term diversification benefits. If we see a catalyst and material change in this trend, we will consider increasing our global allocation from the current underweight positioning.

Fixed income

Our fixed income gauge remains the same, bullish / full exposure with a major tilt toward shorter term duration and to US treasuries. For our UHNW clients in high-tax states, mid-duration municipals are also currently offering tax-adjusted yields.

The dot plot from the Dec Fed meeting projects rate cuts to 4.6% later in 2024 which supports our thesis for riding the higher yielding opportunities for the time being until we see more dramatic shifts in rates.

Private Market Update – Q4/2023

Louis Frank: Partner, Private Market PM

The rising rate environment in 2023 created an opportunity set in private markets.

This disruption proved to be detrimental to some asset classes, while creating opportunities in others.

For example, private equity, venture capital and real estate equity all experienced major stresses. Consider an expected $182B of commercial real estate loans that are set to mature this year (source: Moody’s Analytics, Inc) and need to be refinanced, likely at 2x the rates they had previously been paying.

LotusGroup private investments have largely avoided these asset classes both in our diversified fund offerings as well as direct investments for clients.

On the positive side, rising rates have resulted in opportunities for the specialty finance and credit sectors, two areas that LotusGroup has focused on heavily in recent years.

Deal flow has been steady, and we have remained disciplined as we underwrite our pipeline.

We walk through an income-generating opportunity below.

Telecom Invoice FactoringInvestment Highlights:

Senior secured credit facility to specialized lenders backed by Telecom Companies (Sony, ATT, Verizon, etc.).

75% of the factored invoices are covered by an A- insurance policy written by Allianz (the other 25% are publicly traded TelCo’s)

SOFR + ~9.50% = Approx. 14.8% current total yield as of this writing

1st loss tranche on our investment

Investment Overview: The business is a specialized lender providing liquidity to general contractors servicing telecommunications towers. Cell tower sites are commissioned and maintained by networks or by site management companies, tower companies (such as Crown Castle and American Towers), or original equipment manufacturers (OEMs) such as Nokia or Ericsson. These companies typically sub-contract installation, maintenance, upgrading, and decommissioning to specialized general contractors (GCs). GCs are asset and staff-intensive businesses holding substantial inventory in warehouses.

Investment Structure: This was structured as a co-investment to LotusGroup’s diversified fund program.

The information contained herein, including but not limited to research, market valuations, calculations, estimates, and other material obtained from LotusGroup, and other sources, are believed to be reliable. However, LotusGroup does not warrant its accuracy or completeness. These materials are provided for informational purposes only and should not be used or construed as an offer to sell or a solicitation of an offer to buy any security. Past performance is not indicative of future results.

This blog expresses the views of the author(s) as of the date indicated, and such views are subject to change without notice. Investment advisory services are offered through LotusGroup Advisors, LLC, a federally registered investment adviser. LotusGroup transacts business only in states where it is appropriately registered, excluded, or exempted from registration requirements.The information contained within is believed to be from reliable sources. However, its accuracy, completeness, and the opinions based thereon by the author(s) are not guaranteed – no responsibility is assumed for omissions or errors. The views expressed herein reflect the authors’ judgment now, are subject to change without notice, and may or may not be updated. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must make their own evaluation and investigation of any investments considered or of any investment strategies described herein (including the risks and merits thereof), should seek professional advice for their particular circumstances, and should inform themselves as to the tax or other consequences of any investments or services considered or described herein. LotusGroup’s advisory clients will be required to execute an Investment Advisory Agreement and related Account opening documents (collectively, “Agreements”). If any of the terms or descriptions in this presentation are inconsistent with the terms of the Agreements, such Agreements shall control. Prospective investors should maintain the financial capability and willingness to accept the risks associated with any investments made, should consult the relevant investment prospectus or legal documents, and should their Advisor Representative before making investment decisions (including but not limited to an examination of the investment objectives, risks, charges, and expenses of any investment product(s) considered).

Extracted performance in this presentation is representative of a subset of investments extracted from a portfolio. Such performance is depicted in this presentation based on accounts that match the following criteria: Tactical 100 model held at TD Ameritrade with Moderate Agg risk that includes private investments. LGA employee accounts are excluded from this extracted performance. LGA will provide full performance information promptly upon request. The performance data provided herein is for information and discussion purposes only. The performance of an individual account may vary substantially based on various factors, including, but not limited to, initial account management start date, risk profiles, cash allocation, and investment restrictions, among many others. This information is unaudited. Please refer to an account’s brokerage statement for individual account information. Past performance does not guarantee future results.

To better understand the nature and scope of our advisory services and business practices, readers are encouraged to review via the SEC’s website @ www.adviserinfo.sec.gov, the adviser’s Form ADV Disclosure(s), and the Form ADV 2B Brochure Supplement of each LotusGroup Investment Professional (Click on the link, select “Investment Advisor firm,” and type in the firm name. Results will provide you both Part 1 and 2 of the LotusGroup ‘s Form ADV.).

This blog, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part in any form without our prior written consent.

US Equity:

We ended Q4 as we began with portfolios positioned moderately bullish (75% beta to market), albeit with a couple months mid-quarter in a fully bullish position (100% beta to the market).

We’ll first look at how the market performed in 2023 and then review how we were positioned throughout the year.

The US stock market had a strong performance in 2023.

The performance across the different sectors varied greatly: some sectors had very strong performance (tech), some flat (energy), and some negative (utilities). The return dispersion from the highest return (tech) to the lowest (utilities) was above average compared to years past.

The below chart shows the S&P’s (light pink line) overall performance was mainly driven by a few sectors.

US Equity:

We ended Q4 as we began with portfolios positioned moderately bullish (75% beta to market), albeit with a couple months mid-quarter in a fully bullish position (100% beta to the market).

We’ll first look at how the market performed in 2023 and then review how we were positioned throughout the year.

The US stock market had a strong performance in 2023.

The performance across the different sectors varied greatly: some sectors had very strong performance (tech), some flat (energy), and some negative (utilities). The return dispersion from the highest return (tech) to the lowest (utilities) was above average compared to years past.

The below chart shows the S&P’s (light pink line) overall performance was mainly driven by a few sectors.